Ukraine was the largest recipient of German government arms export licenses in the first half of 2026, with approved exports worth more than EUR 2.52 billion.

Ukraine was the largest recipient of German government arms export licenses in the first half of 2026, with approved exports worth more than EUR 2.52 billion.

As of the morning of July 16, Russian attacks left consumers without electricity in six Ukrainian regions, while nationwide electricity consumption has begun to decline.

As of the morning of July 16, Russian attacks left consumers without electricity in six Ukrainian regions, while nationwide electricity consumption has begun to decline.

Ukrainian President Volodymyr Zelensky has signed a decree enacting a National Security and Defense Council (NSDC) decision to amend the sectoral sanctions imposed on Russian financial institutions.

Ukrainian President Volodymyr Zelensky has signed a decree enacting a National Security and Defense Council (NSDC) decision to amend the sectoral sanctions imposed on Russian financial institutions.

At its meeting, the Cabinet of Ministers approved the privatization terms for the Odesa Port Plant, as well as the sale of two sanctioned assets: the Demurinsky Mining and Processing Plant and Motordetal-Konotop LLC.

At its meeting, the Cabinet of Ministers approved the privatization terms for the Odesa Port Plant, as well as the sale of two sanctioned assets: the Demurinsky Mining and Processing Plant and Motordetal-Konotop LLC.

The updated decision of Ukraine's National Security and Defense Council (NSDC) on sectoral sanctions against Russia's financial sector extends restrictions to virtual assets, digital financial services, and other infrastructure that Russia uses for international transactions to circumvent sanctions.

The updated decision of Ukraine's National Security and Defense Council (NSDC) on sectoral sanctions against Russia's financial sector extends restrictions to virtual assets, digital financial services, and other infrastructure that Russia uses for international transactions to circumvent sanctions.

Ambassadors of EU member states again failed to agree on the final content of the 21st sanctions package against Russia, but they did agree to extend the deadline for the price cap on Russian oil from July 15 to July 23.

Ambassadors of EU member states again failed to agree on the final content of the 21st sanctions package against Russia, but they did agree to extend the deadline for the price cap on Russian oil from July 15 to July 23.

The European Union is planning to continue assisting Ukraine’s energy infrastructure in the light of the Russian attacks ahead of the winter, committing to allocate EUR 920 million to this end.

The European Union is planning to continue assisting Ukraine’s energy infrastructure in the light of the Russian attacks ahead of the winter, committing to allocate EUR 920 million to this end.

The Russian petrochemical complex Gazprom Neftekhim Salavat in the Urals, one of the largest in the country, shut down on Tuesday following an attack by Ukrainian drones.

The Russian petrochemical complex Gazprom Neftekhim Salavat in the Urals, one of the largest in the country, shut down on Tuesday following an attack by Ukrainian drones.

Guardian analysis found the removals coincided with the Trump administration’s push to weaken efficiency rulesAs millions of Americans prepare for another brutal heatwave, it’s now harder to find information about ways to stay cool while saving energy and keeping utility costs down.At least 1,662 Department of Energy webpages offering guidance on protecting the electrical grid during heatwaves have gone dark as of 3 July, according to a Guardian analysis of a list of deleted URLs provided by res

Guardian analysis found the removals coincided with the Trump administration’s push to weaken efficiency rules

As millions of Americans prepare for another brutal heatwave, it’s now harder to find information about ways to stay cool while saving energy and keeping utility costs down.

At least 1,662 Department of Energy webpages offering guidance on protecting the electrical grid during heatwaves have gone dark as of 3 July, according to a Guardian analysis of a list of deleted URLs provided by researchers at the Internet Archive, a non-profit that hosts a repository of more than a trillion archived webpages.

As of the morning of July 15, Russian attacks have left consumers without electricity in four Ukrainian regions, while more than 50 settlements in seven regions remain without power due to severe weather.

As of the morning of July 15, Russian attacks have left consumers without electricity in four Ukrainian regions, while more than 50 settlements in seven regions remain without power due to severe weather.

Ukraine's Russian-occupied Zaporizhzhia Nuclear Power Plant (NPP) has suffered another blackout – its tenth since the beginning of 2026. External power has since been restored.

Ukraine's Russian-occupied Zaporizhzhia Nuclear Power Plant (NPP) has suffered another blackout – its tenth since the beginning of 2026. External power has since been restored.

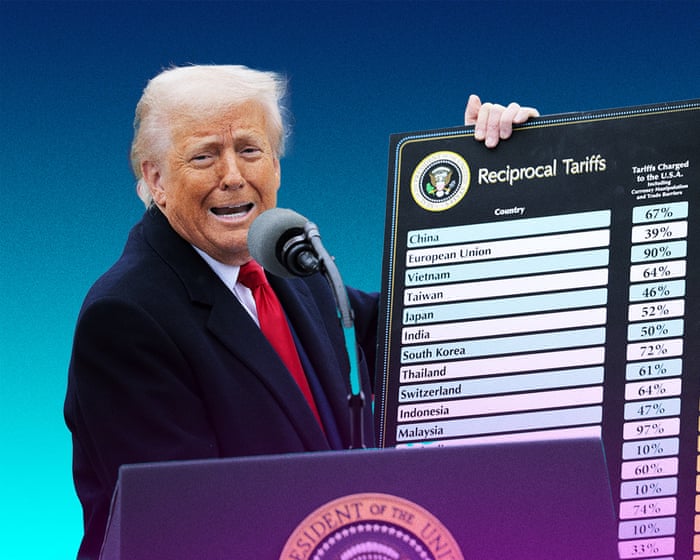

The US government has been forced to pay billions in refunds to companies that were hit by Donald Trump’s ‘liberation day’ tariffs. The US has paid out $81bn (£61bn) this fiscal year after the supreme court ruled the tariffs were illegal. Lucy Hough speaks to international editor Chris Michael Continue reading...

The US government has been forced to pay billions in refunds to companies that were hit by Donald Trump’s ‘liberation day’ tariffs. The US has paid out $81bn (£61bn) this fiscal year after the supreme court ruled the tariffs were illegal. Lucy Hough speaks to international editor Chris Michael

The Verkhovna Rada, Ukraine's parliament, has ratified the Free Trade Agreement (FTA) between the Government of Ukraine and the Government of the Republic of Turkey.

The Verkhovna Rada, Ukraine's parliament, has ratified the Free Trade Agreement (FTA) between the Government of Ukraine and the Government of the Republic of Turkey.

Recent strikes have sent oil prices climbing again, with average gas price per gallon up by $0.70 compared with 2025Inflation cooled to an annual rate of 3.5% in June as the brief US-Iran ceasefire, which has since ended, brought energy prices down, according to new data from the Bureau of Labor Statistics.The consumer price index (CPI), which measures a basket of goods and services, has been elevated since the start of the war, largely because of higher energy prices. After mostly staying under

Recent strikes have sent oil prices climbing again, with average gas price per gallon up by $0.70 compared with 2025

Inflation cooled to an annual rate of 3.5% in June as the brief US-Iran ceasefire, which has since ended, brought energy prices down, according to new data from the Bureau of Labor Statistics.

The consumer price index (CPI), which measures a basket of goods and services, has been elevated since the start of the war, largely because of higher energy prices. After mostly staying under 3% since mid-2024, CPI reached a three-year high of 4.2% in May – up from 2.4% in February. Month-over-month, CPI fell 0.8% in June, the largest one-month decrease since April 2020.

Energy prices later stabilise after Trump abandons plan for 20% levy on traffic through strait of Hormuz Oil and gas prices jumped and expectations of interest rate rises in Europe increased on Tuesday after the US carried out a third night of military strikes against Iran.However, they later eased back after Donald Trump said he would abandon his proposal for the US to levy a 20% fee on cargo passing through the strait of Hormuz. Continue reading...

However, they later eased back after Donald Trump said he would abandon his proposal for the US to levy a 20% fee on cargo passing through the strait of Hormuz.

As of the morning of July 14, Russian attacks left consumers without electricity in seven regions of Ukraine, while 72 settlements in three regions remained without power due to severe weather.

As of the morning of July 14, Russian attacks left consumers without electricity in seven regions of Ukraine, while 72 settlements in three regions remained without power due to severe weather.

Russia’s State Duma has passed the largest overhaul of its bankruptcy law since the statute was written. On paper, the reform saves jobs by favoring rescue over liquidation.

It hands the Kremlin a legal instrument to decide which companies survive the insolvency wave.

In practice, Ukraine’s foreign intelligence assesses, it hands the Kremlin a legal instrument to decide which companies survive the insolvency wave building inside Russia’s war economy—a state-run ver

Russia’s State Duma has passed the largest overhaul of its bankruptcy law since the statute was written. On paper, the reform saves jobs by favoring rescue over liquidation.

It hands the Kremlin a legal instrument to decide which companies survive the insolvency wave.

In practice, Ukraine’s foreign intelligence assesses, it hands the Kremlin a legal instrument to decide which companies survive the insolvency wave building inside Russia’s war economy—a state-run version of “too big to fail,” where Moscow writes the list.

The fine print lets Moscow overrule creditors

The scale explains the urgency. Russian companies now owe more than everything Russia’s economy produces annually: 293 trillion rubles ($3.85 trillion) in liabilities by the end of April, against a GDP of about 214 trillion rubles ($2.8 trillion). Overdue payments rose 18% in a year to 7 trillion rubles ($92 billion).

That unpaid sum equals roughly three-quarters of Russia’s official annual defense budget. More than a third of corporate profits now go to paying interest alone.

In a system where the biggest lenders are state banks, that lets Moscow impose survival on chosen enterprises.

The law flips the system’s default from liquidation to rescue. Companies gain a pre-bankruptcy sanation track to settle with creditors before any court case opens, plus a judicial debt-restructuring procedure with plans running up to four years, extendable by four more. A new anti-crisis manager oversees the debtor’s finances, payments, and recovery plan.

The decisive mechanism is the binding clause. For large debtors—companies with assets above 1 billion rubles ($13 million)—a court-approved sanation agreement, backed by a majority of independent creditors, becomes binding even on creditors who refuse to sign it. In a system where the biggest lenders are state banks, that lets Moscow impose survival on chosen enterprises and silence holdouts.

Six years of stalling ended in two days

Versions of this reform stalled for six years, with one government bill frozen in the Duma for two and a half years. Then the package cleared its second reading on 7 July and passed the third a day later.

“Its hasty advancement coincided with a sharp deterioration in Russian companies’ finances,” Ukraine’s Foreign Intelligence Service assessed on 13 July. The system being replaced rescued almost no one: external administration was applied in 51 cases in all of 2025, financial recovery in eight, and rehabilitation accounted for less than 1% of corporate bankruptcies.

Sberbank chief German Gref told shareholders in late June that investment had fallen more than 14% and could drop a further 3% this year.

The agency expects Moscow to apply the new mechanisms selectively—defense plants first, then critical infrastructure, large employers, and companies dependent on state orders—to stagger big insolvencies and keep distressed assets from flooding the market at once.

Russia’s own top financiers had already publicly linked the strain to the war. Sberbank chief German Gref told shareholders in late June that investment had fallen more than 14% and could drop a further 3% this year, while central bank governor Elvira Nabiullina’s Bank of Russia conceded that pro-inflationary risks had worsened.

Explore further

Russia’s top bankers break taboo, admit war is hurting the economy

The warnings are not only Ukrainian. In February, Ukrainian intelligence put non-performing loans above the 11% threshold that defines a systemic banking crisis, citing research on the $210–250 billion in loans Russian banks were forced to extend to defense contractors.

And a European intelligence note seen by Reuters warned on 6 July that the burden banks carry for the war economy creates an “explosive” risk—more than 500,000 Russians declared personal bankruptcy in 2025, up almost a third in a year.

Russian bankruptcy practitioners caution the new procedure works only if courts genuinely assess whether a business can recover.

Russian bankruptcy practitioners caution the new procedure works only if courts genuinely assess whether a business can recover—and with over a third of profits going to interest, many cannot. The law postpones the reckoning rather than canceling it.

Poland does not currently see any possibility of lifting its unilateral ban on imports of certain Ukrainian agricultural products, arguing that doing so would harm the country's agricultural market and local producers.

Poland does not currently see any possibility of lifting its unilateral ban on imports of certain Ukrainian agricultural products, arguing that doing so would harm the country's agricultural market and local producers.

The United Kingdom has agreed to contribute to the European Union’s loan program supporting Ukraine in 2026–2027, with its contribution corresponding to the value of contracts signed with UK defence manufacturers.

The United Kingdom has agreed to contribute to the European Union’s loan program supporting Ukraine in 2026–2027, with its contribution corresponding to the value of contracts signed with UK defence manufacturers.

As of the morning of July 13, Russian strikes have left users without power in three regions; due to severe weather, 29 settlements in two regions remain without electricity.

As of the morning of July 13, Russian strikes have left users without power in three regions; due to severe weather, 29 settlements in two regions remain without electricity.

Gasoline prices in Russia are rising rapidly amid intensified Ukrainian long-range strikes on Russian oil refineries and other fuel infrastructure facilities.

Gasoline prices in Russia are rising rapidly amid intensified Ukrainian long-range strikes on Russian oil refineries and other fuel infrastructure facilities.

Ukraine has received $3.35 billion into its state budget under the First Ukraine Jobs and Private Sector Growth Development Policy Operation, implemented jointly with the World Bank.

Ukraine has received $3.35 billion into its state budget under the First Ukraine Jobs and Private Sector Growth Development Policy Operation, implemented jointly with the World Bank.

After a 10-day clock, the housing bill turned into law at midnight without the president’s signature. But his decision not to sign reflects a growing rift between him and Senate Republicans.

After a 10-day clock, the housing bill turned into law at midnight without the president’s signature. But his decision not to sign reflects a growing rift between him and Senate Republicans.

President Trump with Senator John Thune, the majority leader, at the Capitol last month, on the day he had been set to sign the bipartisan housing bill.

German defense technology company Quantum Systems has signed a multimillion-euro contract to supply Ukraine with ten autonomous Daimler Truck Zetros vehicles and ten MANDRILL unmanned ground platforms for frontline testing.

German defense technology company Quantum Systems has signed a multimillion-euro contract to supply Ukraine with ten autonomous Daimler Truck Zetros vehicles and ten MANDRILL unmanned ground platforms for frontline testing.

German companies DEUTZ and ARX Robotics are launching industrial-scale serial production of Gereon unmanned ground systems in the city of Ulm, with the first units expected to be delivered to Ukraine by the end of the summer.

German companies DEUTZ and ARX Robotics are launching industrial-scale serial production of Gereon unmanned ground systems in the city of Ulm, with the first units expected to be delivered to Ukraine by the end of the summer.

As of the morning of July 10, Russian attacks left consumers without electricity in four Ukrainian regions, while severe weather continued to disrupt power supply in ten settlements across two regions.

As of the morning of July 10, Russian attacks left consumers without electricity in four Ukrainian regions, while severe weather continued to disrupt power supply in ten settlements across two regions.

Ukraine is interested in cooperating with Japan's Mitsubishi, which holds a license to manufacture missiles for the Patriot air defense system and has experience in establishing such production.

Ukraine is interested in cooperating with Japan's Mitsubishi, which holds a license to manufacture missiles for the Patriot air defense system and has experience in establishing such production.

The Japan International Cooperation Agency (JICA) has launched the Japan-Ukraine Tech Co-Creation Project, a new initiative aimed at fostering partnerships between Ukrainian and Japanese technology companies.

The Japan International Cooperation Agency (JICA) has launched the Japan-Ukraine Tech Co-Creation Project, a new initiative aimed at fostering partnerships between Ukrainian and Japanese technology companies.

As of the morning of July 9, Russian attacks left consumers without electricity in five Ukrainian regions, while another 168 settlements in four regions remained without power due to bad weather.

As of the morning of July 9, Russian attacks left consumers without electricity in five Ukrainian regions, while another 168 settlements in four regions remained without power due to bad weather.

Russian Deputy Prime Minister Alexander Novak announced at a government meeting with Kremlin leader Vladimir Putin that Russia had imposed a ban on diesel exports effective July 8.

Russian Deputy Prime Minister Alexander Novak announced at a government meeting with Kremlin leader Vladimir Putin that Russia had imposed a ban on diesel exports effective July 8.

Ukraine has begun implementing 29 water supply projects under its regional resilience plans, with the initiatives expected to provide reliable water access to more than ten million people.

Ukraine has begun implementing 29 water supply projects under its regional resilience plans, with the initiatives expected to provide reliable water access to more than ten million people.

Even voters who identify as foot soldiers of his political army are increasingly willing to blame Trump for their economic troublesThe political consequences of Donald Trump’s policy mayhem are now coming into view: “Maga” America is getting pissed.It has been a sight to see how every one of the president’s policy initiatives has sabotaged some core constituency or other. From farmers and rural Americans to manufacturing workers and every American struggling to make ends meet, Trump has torched

Even voters who identify as foot soldiers of his political army are increasingly willing to blame Trump for their economic troubles

The political consequences of Donald Trump’s policy mayhem are now coming into view: “Maga” America is getting pissed.

It has been a sight to see how every one of the president’s policy initiatives has sabotaged some core constituency or other. From farmers and rural Americans to manufacturing workers and every American struggling to make ends meet, Trump has torched pretty much his entire political base. For all his efforts to rig the midterm elections in his favor, it’s as if he is daring the Maga faithful to drop him.

As of the morning of July 8, Russian attacks had left additional consumers without electricity in six Ukrainian regions, while severe weather continued to disrupt power supply to ten settlements in the Khmelnytskyi region.

As of the morning of July 8, Russian attacks had left additional consumers without electricity in six Ukrainian regions, while severe weather continued to disrupt power supply to ten settlements in the Khmelnytskyi region.

About 57% of polled Americans also believe economy is worsening in grim portrait of cost of living crisis, according to Harris survey for the GuardianNinety-five per cent of Americans believe the US is suffering an affordability crisis, as many report trouble with the rising cost of groceries and gas, according to an exclusive new poll conducted for the Guardian.The survey, conducted by Harris Poll, paints a bleak picture of how people feel about the US economy amid the war in Iran and ahead of

About 57% of polled Americans also believe economy is worsening in grim portrait of cost of living crisis, according to Harris survey for the Guardian

Ninety-five per cent of Americans believe the US is suffering an affordability crisis, as many report trouble with the rising cost of groceries and gas, according to an exclusive new poll conducted for the Guardian.

The survey, conducted by Harris Poll, paints a bleak picture of how people feel about the US economy amid the war in Iran and ahead of the key midterm elections this fall.

Two of Russia's most senior economic figures publicly linked the country's mounting economic pressures to the war in Ukraine last week — an unusual departure from the official silence that has surrounded Kremlin war costs since 2022. German Gref, chief executive of Sberbank, and central bank governor Elvira Nabiullina both spoke in separate settings as Ukraine's drone strike campaign against Russian oil infrastructure compounds the fiscal strain from record military spendin

Two of Russia's most senior economic figures publicly linked the country's mounting economic pressures to the war in Ukraine last week — an unusual departure from the official silence that has surrounded Kremlin war costs since 2022. German Gref, chief executive of Sberbank, and central bank governor Elvira Nabiullina both spoke in separate settings as Ukraine's drone strike campaign against Russian oil infrastructure compounds the fiscal strain from record military spending.

Russia's military and classified spending reached 46% of all budget expenditure in the first quarter of 2026 — a surge of roughly 30% over the same period in 2025 — while the National Wealth Fund buffer has fallen from about 7% of GDP before the war to 1.7% as of April 2026, Russia's Finance Ministry confirmed.

What each of them said

Gref told Sberbank's annual shareholders meeting that investments had already fallen over 14% and could drop a further 3% this year. He then addressed the war directly.

"I don't believe there is anyone in this country whose primary concern is anything other than an end to military hostilities as soon as possible," Gref said.

For the chief executive of Russia's largest state-controlled bank to frame the war as the country's overriding problem — not "the special military operation," not a security challenge to be managed — marks a notable break from the language Kremlin officials have enforced since February 2022.

Nabiullina's public position is more constrained, but the Bank of Russia's own press release on her June rate decision said fiscal policy had become more accommodative than previously expected and that pro-inflationary risks had worsened — the same dynamic that Kluge's analysis traces directly to the gap between military outlays and tax revenues.

The fiscal picture behind the exchange

The 46% military spending figure comes from analyst Janis Kluge of the German Institute for International and Security Affairs, drawn from Finance Ministry data and cited by ISW. Russia is now covering an increasing share of the deficit through borrowing, with liquid National Wealth Fund assets depleted to a fraction of their pre-war level and no longer functioning as a meaningful cushion.

Ukraine's strike campaign is compressing the revenue side simultaneously. Bloomberg counted 38 Ukrainian strikes on Russian refineries from January through May 2026, with 16 in May alone — the highest monthly figure of the war. Two strikes on 16 and 18 June disabled both primary processing units at the Kapotnya refinery in Moscow — the capital's main fuel source — leaving it unable to process crude until at least early 2027.

Russia has responded by banning gasoline and jet fuel exports, drawing down strategic reserves, allowing lower-grade fuel blends, and importing gasoline from India and Belarus, while negotiations with Kazakhstan are complicated by the fact that a Ukrainian strike disrupted the feedstock supply to one potential Kazakh supplier.

Russian President Valdimir Putin publicly admitted queues at filling stations while summoning top officials to manage the crisis. Parliament passed legislation subsidizing gasoline imports from abroad.

The country’s unemployment rate dropped slightly to 4.2% as US job growth also slowed for the monthSign up for the Breaking News US newsletter emailUS job growth slowed in June as employers added 57,000 new jobs – just about half of what economists had predicted – and the Bureau of Labor Statistics revised its figures from the past two months down by a total of 74,000.The country’s unemployment rate dropped slightly to 4.2%, but the number of unemployed people changed little, according to the la

US job growth slowed in June as employers added 57,000 new jobs – just about half of what economists had predicted – and the Bureau of Labor Statistics revised its figures from the past two months down by a total of 74,000.

The country’s unemployment rate dropped slightly to 4.2%, but the number of unemployed people changed little, according to the latest data, as 720,000 people left the labor force. The bureau revised the unexpectedly high May figures from 172,000 new jobs to 129,000, and revised the April figures from 179,000 to 148,000.

A housing shortfall, record home costs and cuts to subsidies are intensifying the US affordability crunchOf the various dimensions of the affordability crisis weighing on US families, housing probably weighs heaviest. The typical home price has risen above five times the annual income of the typical family. The monthly cost of owning a home has hit record highs.The US faces a housing shortfall of millions of homes. But builders are not rushing to meet the shortfall. The supply of new homes decli

A housing shortfall, record home costs and cuts to subsidies are intensifying the US affordability crunch

Of the various dimensions of the affordability crisis weighing on US families, housing probably weighs heaviest. The typical home price has risen above five times the annual income of the typical family. The monthly cost of owning a home has hit record highs.

The US faces a housing shortfall of millions of homes. But builders are not rushing to meet the shortfall. The supply of new homes declined over 14% in May, compared to May of 2025. Moody’s Analytics expects single-family and multifamily residential investment to contract every year between now and 2030.

The European Union renewed its economic sanctions on Russia for another 12 months, to 31 July 2027, the Council of the EU said on 25 June. The decision keeps the bloc's full economic regime against Moscow in place over the war on Ukraine. It follows the agreement EU leaders reached at their June summit.

The EU first imposed these economic measures in 2014 over Russia's full-scale invasion of Ukraine, then sharply widened them after the full-scale invasion in February 2022.

The European Union renewed its economic sanctions on Russia for another 12 months, to 31 July 2027, the Council of the EU said on 25 June. The decision keeps the bloc's full economic regime against Moscow in place over the war on Ukraine. It follows the agreement EU leaders reached at their June summit.

The EU first imposed these economic measures in 2014 over Russia's full-scale invasion of Ukraine, then sharply widened them after the full-scale invasion in February 2022. Brussels has cast the renewal as keeping pressure on Moscow until it stops the war and negotiates.

What the renewed measures cover

The sanctions span trade, finance, energy, and dual-use technology, the Council said. They include the ban on importing or transferring Russian seaborne crude oil and certain petroleum products into the EU.

They also bar transactions with several Russian financial institutions and crypto service providers, including some based in third countries, and suspend the broadcasting licenses of several Kremlin-backed disinformation outlets in the EU. Other tools let the bloc counter attempts to circumvent the sanctions.

The Council said the EU would keep the measures in place and stood ready to add more as long as Russia continues its war.

Explore further

Russia’s former soldiers may face a locked EU border—if France and Italy stop balking

Part of a wider sanctions push

The renewal builds on a regime that now spans 20 sanctions packages adopted since the February 2022 invasion. The bloc's leaders had agreed to the 12-month extension at the European Council on 18–19 June, when one member state's pro-Russian leader had vowed to veto the next batch.

EU leaders also called for swift adoption of a 21st sanctions package, aimed at further cutting Russia's energy revenue, curbing its shadow fleet, and constraining its banks. The renewal lands as enforcement draws scrutiny elsewhere: Washington has removed a string of Russians, ships, and firms from its own blacklist in recent months, giving no public reason.

Alongside the economic measures, the EU keeps separate restrictions on occupied Crimea, including Sevastopol, and on the Russian-occupied parts of the Donetsk, Kherson, Luhansk, and Zaporizhzhia oblasts, plus asset freezes and travel bans on a broad list of individuals and entities.

On 22 June, Volodymyr Zelenskyy signed a record budget of 4.4 trillion hryvnia ($97.6 billion), most of it borrowed from Europe. The money to keep Ukraine fighting, and eventually to rebuild it, is flowing as never before.

The constraint that now shapes Ukraine’s economic future is no longer money but the power, workers, and institutions to use it.

That same quarter, the economy it is meant to revive posted its sharpest contraction since the wartime recovery began—

On 22 June, Volodymyr Zelenskyysigned a record budget of 4.4 trillion hryvnia ($97.6 billion), most of it borrowed from Europe. The money to keep Ukraine fighting, and eventually to rebuild it, is flowing as never before.

The constraint that now shapes Ukraine’s economic future is no longer money but the power, workers, and institutions to use it.

That same quarter, the economy it is meant to revive posted its sharpest contraction since the wartime recovery began—and the constraint that now shapes Ukraine’s economic future is no longer money but the power, workers, and institutions to use it.

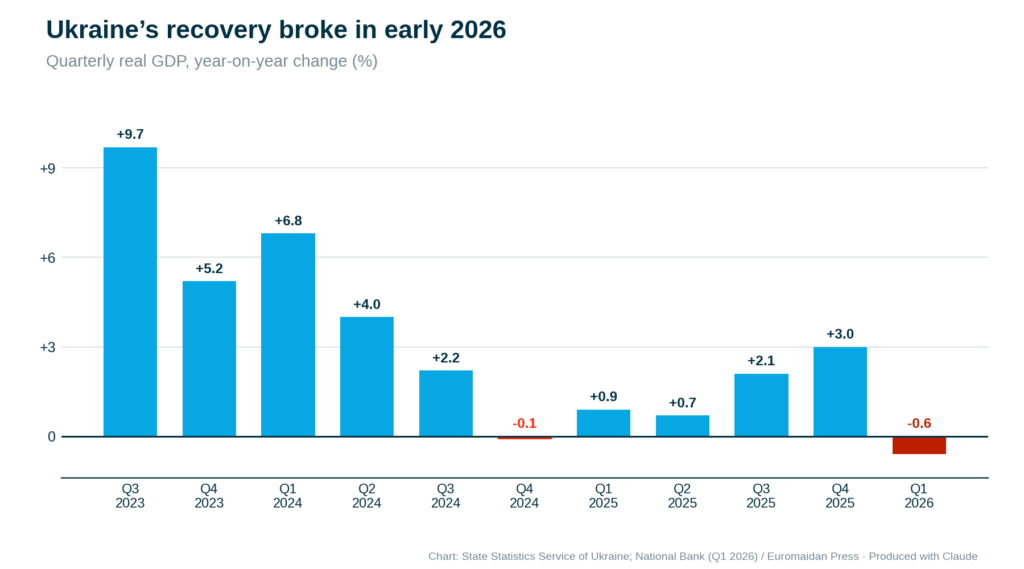

Real GDP fell 0.6% year-on-year in the first quarter of 2026, the National Bank confirmed on 18 June, and 0.7% against the previous quarter. The number is small. What hides behind it is not.

For nearly three years, Ukraine’s economy grew through bombardment—near-continuously from the middle of 2023, when the country clawed its way back from a collapse of almost 29% in the invasion year. It dipped only once before now, briefly, when drought hammered the harvest at the end of 2024. The first quarter of 2026 was the sharper break.

The investment house ICU said it bluntly: weak growth is “the new norm.”

The official line is more hopeful: the National Bank expects growth back as soon as the second quarter, and the government pencils in 4.5% for 2027. But a bounce off a depressed quarter is not a recovery, and the full-year number has only been marked down further.

After the recovery took hold in mid-2023, Ukraine’s economy grew nearly every quarter, dipping only once—a marginal 0.1% when drought gutted the 2024 harvest. Russia’s strike campaign then pushed it down 0.6% year-on-year in the first quarter of 2026. Chart: State Statistics Service of Ukraine; National Bank of Ukraine / Euromaidan Press. Produced with Claude

Where the bombs show up in the accounts

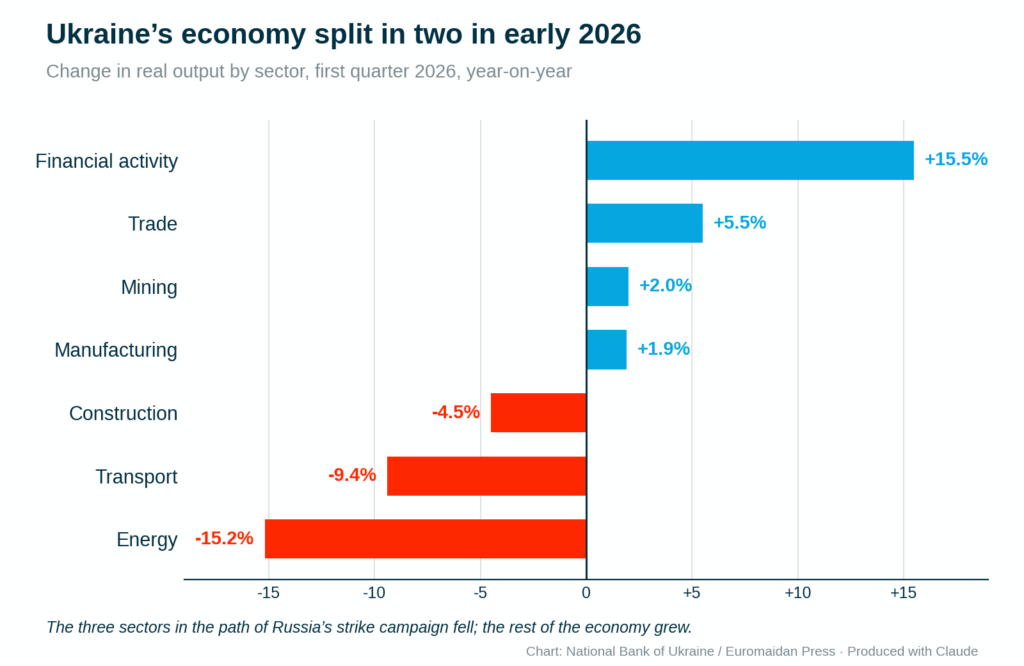

The contraction has a clear author. Energy output fell 15.2% year-on-year, transport 9.4%, and construction 4.5%, the National Bank’s breakdown showed—the sectors directly in the path of the strike campaign, now showing up as line items in the national accounts.

The economy contracted because three bombed sectors outweighed a domestic economy that kept working.

The first sector to fall was electricity generation, with transmission disrupted where the grid was hit; the second was transport, after heavy strikes on the railways, economist Oleksandra Betliy told Kyiv Post.

Household consumption rose 11%. Manufacturing grew 1.9%, trade 5.5%, financial activity 15.5%, and mining 2%. The economy contracted because three bombed sectors outweighed a domestic economy that, by almost every other measure, kept working. ICU called the quarter a display of “unprecedented resilience” to the blackouts.

The hryvnia keeps sliding

Unlike the contraction, the hryvnia's slide owes nothing to the weather. Through the first five months of 2026, the hryvnia weakened against the National Bank’s official rate—from a 2025 average of 41.7 to the dollar to 42.9 in January, 44.1 by May, and 44.9 by 23 June. A widening trade gap drives the slide, the Centre for Economic Strategy reported.

A cold snap can knock out a quarter of GDP growth. It cannot make a currency depreciate every month for half a year. That slide tracks a structural deficit between what Ukraine earns abroad and what it spends there, and it will outlast the spring.

Reserves dropped to $45.7 billion by the start of June.

Defending that slide has cost the central bank its cushion. Reserves dropped to $45.7 billion by the start of June, down from a record near $57.7 billion early in the year—roughly $12 billion sold off in four months to slow the hryvnia while partner aid ran late. The National Bank calls the level sufficient, about 4.7 months of imports, and the inflows now arriving are meant to refill it.

Prices, at least, are easing. Inflation slowed to 8.2% in May, helped by falling oil prices as the war in the Middle East de-escalated—Washington cleared Iranian crude sales on 22 June, pushing prices to around $74 a barrel, which both cheapens Ukraine’s energy imports and thins Russia’s war revenue. The National Bank held its key rate at 15% on 18 June, judging the easing cycle done for now.

The contraction came from three sectors, not the whole economy. Energy, transport, and construction—the parts directly in the path of Russia’s strikes—fell sharply in the first quarter of 2026, while financial activity, trade, mining, and manufacturing kept growing. Chart: National Bank of Ukraine / Euromaidan Press. Produced with Claude

The deeper drag

The contraction had near-term authors—the strikes, the cold, the delayed budget spending. The drag beneath them is older, and no thaw fixes it: Ukraine is running out of people. The number of full-time employees fell from 7 million in 2021 to 5.3 million by late 2025, according to GMK Center, citing official data.

The shortage pushes wages up even as output falls—part of why inflation has stayed above 8%.

Half of companies were already citing the staff shortage as the main obstacle to their businesses six months ago, Euromaidan Press reported, citing the National Bank’s enterprise survey, and the labor force has only thinned since then.

The war took around a quarter of the labor force; 5.9 million Ukrainians are abroad; and the National Bank expects the net outflow to run into 2027 before any return begins. The shortage pushes wages up even as output falls—part of why inflation has stayed above 8%, and a large part of why every forecaster now caps growth near zero.

Explore further

How Ukraine’s economy survived four years of war—and what it cost

Money is arriving

For most of the war, the binding question was whether the money would come at all. In February, it nearly didn’t: Hungary’s Viktor Orbán blocked the €90 billion ($104 billion) EU loan agreed in December, holding it hostage to a dispute over Russian oil through the Druzhba pipeline.

Then Orbán lost his election after 16 years; his successor dropped the obstruction; the pipeline was repaired; and the bloc finally approved the package on 23 April—€45 billion ($52 billion) of it for 2026.

The inflows have a paradoxical effect on the books: the projected 2026 deficit has narrowed to 12.1% of GDP.

That money is what funds the record defense budget. The first €3.2 billion ($3.7 billion) tranche of budget support lands at the Recovery Conference in Gdańsk on 25–26 June, with €5.9 billion ($6.8 billion) for the army to follow by the end of the month, European Pravda reported.

The central bank expects roughly $13 billion in June across all programs. The inflows have a paradoxical effect on the books: the projected 2026 deficit has narrowed to 12.1% of GDP, from the 18.5% first planned, the Centre for Economic Strategy noted in the same review, though defense spending is running at only about 80% of plan, and the budget underfunded the military pay raises it promised.

The bind is no longer the money

The bill, as of December 2025, is almost $588 billion—nearly three times the country’s annual output—a joint assessment estimated by the World Bank, EU, and UN in February, up from the $524 billion figure of a year earlier.

$20 billion to replace destroyed capital, $10 billion to stop falling further behind its eastern European peers, and $10 billion to start closing the gap.

To rebuild and keep pace with its neighbors, Ukraine needs around $40 billion a year, the Berkeley economists Yuriy Gorodnichenko and Maurice Obstfeld estimate: $20 billion to replace destroyed capital, $10 billion to stop falling further behind its eastern European peers, and $10 billion to start closing the gap. Set against Poland’s post-communist investment inflows, or the immobilized Russian assets sitting in Europe, that figure is not a fantasy.

The problem is the other side of the ledger. Ukraine can realistically absorb $10 to 15 billion a year right now, Ukraine’s deputy representative at the IMF, Vladyslav Rashkovan, arguedon a Centre for Economic Strategy podcast.

If $100 billion arrived this month, he said, the country could not spend it. Not enough projects are ready. Not enough institutions to run them. Not enough throughput at a customs service that would have to clear 10 times the imports.

The question now is whether Ukraine can build the capacity to take the funding.

The workers to do the rebuilding are scarcer still: around 4.5 million will be needed, the Economy Ministry projectedalready in January, in an economy already short more than 600,000 skilled hands this year.

The constraint has quietly flipped. For three years, the question was whether the world would fund Ukraine. The question now is whether Ukraine can build the capacity to take the funding—and that is slower, less photogenic work than wiring a loan.

It is also the work that decides everything downstream. Investment does not go where a president points it, Rashkovan said; it goes where the balance of risk and return beats the alternatives. The institutions, the rule of law, the energy capacity to power a rebuilt economy, the workers to build it—none of it visible, all of it now the binding constraint on whether the recovery resumes or settles into the new normal ICU described.

Ukraine has $5.8 billion lined up for priority reconstruction projects this year, and a $9.5 billion funding gap remains.

The contraction may not be the most important number from this June. Ukraine has $5.8 billion lined up for priority reconstruction projects this year, and a $9.5 billion funding gap remains. The bombs are still landing on the sectors that fell. And the hryvnia, indifferent to the weather, keeps closing on 45.

The European Commission is discussing with EU member states various options to cover Ukraine's budget deficit for next year, which could range from $8 billion to $19 billion, the Financial Times reported on July 8.International partners have provided Ukraine with over $39 billion for its wartime economy so far this year, Prime Minister Denys Shmyhal announced.The financial hole in Ukraine's budget is linked to reduced U.S. support and the lack of prospects for a swift ceasefire with Russia that

The European Commission is discussing with EU member states various options to cover Ukraine's budget deficit for next year, which could range from $8 billion to $19 billion, the Financial Times reported on July 8.

International partners have provided Ukraine with over $39 billion for its wartime economy so far this year, Prime Minister Denys Shmyhal announced.

The financial hole in Ukraine's budget is linked to reduced U.S. support and the lack of prospects for a swift ceasefire with Russia that Europe had hoped for, the Financial Times reported.

A senior EU official told the publication that many of Ukraine's partners had previously counted on a peace deal in 2025, but are now forced to revise their funding plans.

This includes the European Commission, which has already adjusted spending from Ukraine-related funding streams.

Without support from Western partners, Kyiv would face a budget deficit of $19 billion in 2026, according to the Financial Times. However, even if additional international financing for the wartime economy can be secured, a gap of at least $8 billion would remain.

To support Ukraine's budget, Europe is considering providing military aid in the form of off-budget grants that would be recorded separately as external transfers but would count toward NATO member countries' national defense spending targets.

One EU diplomat told the Financial Times that military support for Ukraine is viewed as a contribution to the defense of all of Europe.

In a document for G7 countries reviewed by Financial Times, Kyiv proposed that European allies co-finance Ukrainian forces, framing this as a service to strengthen continental security.

Other support options under discussion include potentially accelerating payments from the existing $50 billion G7 loan program and reinvesting frozen Russian assets in higher-yield financial instruments that the EU allocated to help service the debt.

According to the Financial Times, two sources confirmed that the commission planned to discuss these options with EU finance ministers on July 8.

The funding issue will also be raised at the Ukraine Recovery Conference in Rome on July 10-11, dedicated to Ukraine's reconstruction needs. European Commission President Ursula von der Leyen will attend the event.

Russia's economy, which defied initial sanctions and saw growth propelled by massive military spending and robust oil exports, is now showing significant signs of a downturn. Recent economic indicators are flashing red, with manufacturing activity declining, consumer spending tightening, and inflation remaining stubbornly high, straining the national budget, the Wall Street Journal (WSJ) reported on July 4. Russian officials are openly acknowledging the risks of a recession. Economy Minister Max

Russia's economy, which defied initial sanctions and saw growth propelled by massive military spending and robust oil exports, is now showing significant signs of a downturn.

Recent economic indicators are flashing red, with manufacturing activity declining, consumer spending tightening, and inflation remaining stubbornly high, straining the national budget, the Wall Street Journal (WSJ) reported on July 4.

Russian officials are openly acknowledging the risks of a recession. Economy Minister Maxim Reshetnikov warned last month that Russia was on the "verge of a recession," while Finance Minister Anton Siluanov described the situation as a "perfect storm." Companies, from agricultural machinery producers to furniture makers, are reducing output. The central bank announced on July 3 it would debate cutting its benchmark interest rate later this month, following a reduction in June.

While analysts suggest this economic sputtering is unlikely to immediately alter President Vladimir Putin’s war objectives—as his focus on "neutering Ukraine" overrides broader economic concerns—it exposes the limits of his war economy.

The slowdown indicates that Western sanctions, though not a knockout blow, are increasingly taking a toll. If sanctions intensify further or global oil prices fall, Russia’s economy could face more severe instability. This downturn undermines Putin's strategic bet that Russia can financially outlast Ukraine and its Western allies, suggesting Moscow may struggle to finance the war indefinitely.

Experts warn that Russia's economic growth model, overly reliant on military spending, is unsustainable and necessitates a contraction of civilian economic capacities to free up workers for the war machine, which is not a viable long-term strategy. Putin recently dismissed suggestions that the war is stifling the economy, echoing Mark Twain by stating reports of its death "are greatly exaggerated." However, he also cautioned that a recession or stagflation "should not be allowed under any circumstances."

After a brief recession in 2022, military spending, which accounts for over 6% of gross domestic product this year (the highest since Soviet times) and approximately 40% of total government spending, had propped up Russia’s economy and blunted the impact of Western sanctions. Russia’s ability to reroute oil exports to China and Beijing’s support with electronics and machinery provided additional economic stimulus. This created an economic paradox: the most sanctioned major economy was, for a period, growing faster than many advanced economies.

However, this military spending "sugar rush" fueled runaway inflation, compelling the central bank to raise interest rates to a record 21% to try and tame it. Higher interest rates increased borrowing costs for businesses, curbing investment, expansion plans, and squeezing profits. The economic comedown has already begun.

Official data shows Russian GDP growth slowed to 1.4% in the first quarter compared to a year earlier, down significantly from 4.5% in the fourth quarter of 2024. S&P Global’s purchasing managers’ index indicated Russia’s manufacturing sector contracted at its sharpest rate in over three years in June, and new car sales dropped nearly 30% year-over-year in June.

Businesses across Russia are feeling the effects, according to the WSJ. Rostselmash, the country’s largest producer of agricultural machinery, announced in May it would cut production and investment, and pull forward mandatory annual leave for its 15,000 employees due to a lack of demand. In Siberia, electricity grid operator Rosseti Sibir stated it was on the verge of bankruptcy due to high debt, halting investments and proposing tariff hikes for industrial users.

While some analysts argue the Russian banking system remains stable, others warn of increasing instability. A recent report by the Washington, D.C.-based Center for Strategic and International Studies (CSIS) highlighted risks from a government decision to control war-related lending at major Russian banks. The state could direct banks to offer preferential loans, potentially forcing the government to absorb losses if high interest rates prevent companies from meeting obligations.

The Moscow-based Center for Macroeconomic Analysis and Short-Term Forecasting also assessed in May that the risk of a protracted systemic banking crisis in 2026 was "moderate" and growing.

These economic challenges intensify pressure on the Kremlin by reducing its financial capacity to fund its war in Ukraine. The government has operated with a budget deficit throughout the war and projects this will continue for at least two more years. This fiscal strain could provide an opening for Western nations to implement more powerful sanctions.

Falling oil prices present another significant risk for Russia, as energy sales account for about a third of its budget revenues. The price of Russian crude has consistently remained below the level assumed in this year’s budget, and Russia’s oil-and-gas revenue in June fell to its lowest level since January 2023, according to Finance Ministry data.

BlackRock, a U.S. investment firm, suspended work on a multibillion-dollar Ukraine recovery fund following U.S. President Donald Trump's election victory, prompting France to work on a replacement, Bloomberg reported on July 5.The plan nearly secured the initial support of institutions backed by the governments of Germany, Italy, and Poland, people familiar with the matter told Bloomberg.Kyiv has sought to secure investment in Ukraine's reconstruction as Russia's war continues to destroy infrast

BlackRock, a U.S. investment firm, suspended work on a multibillion-dollar Ukraine recovery fund following U.S. President Donald Trump's election victory, prompting France to work on a replacement, Bloomberg reported on July 5.

The plan nearly secured the initial support of institutions backed by the governments of Germany, Italy, and Poland, people familiar with the matter told Bloomberg.

Kyiv has sought to secure investment in Ukraine's reconstruction as Russia's war continues to destroy infrastructure across the country.

BlackRock halted its search for institutional investors in January, causing the planned funding that sought to secure $500 million from governments, development grants, and investment banks, and another $2 billion from private investors, to fall through.

The investment firm halted talks with institutional investors in January due to a lack of interest amid perceived uncertainty in Ukraine.

The fund was set to be unveiled by BlackRock at the upcoming Ukraine Recovery Conference on July 10-11 in Rome, Bloomberg reported.

A spokesperson for BlackRock said the investment firm completed advisory work for the recovery fund pro bono in 2024 and no longer has "any active mandate."

France is working on a proposal to replace the recovery fund led by BlackRock, people familiar with the matter told Bloomberg, adding that it remains uncertain how effective the plan will be without Washington's backing.

President Volodymyr Zelensky and Italian Prime Minister Giorgia Meloni are expected to attend the Ukraine Recovery Conference next week.

Despite a partial rebound from a 30% economic slump in 2022, foreign investment in Ukraine remains underwhelming.