Russia’s State Duma has passed the largest overhaul of its bankruptcy law since the statute was written. On paper, the reform saves jobs by favoring rescue over liquidation.

It hands the Kremlin a legal instrument to decide which companies survive the insolvency wave.

In practice, Ukraine’s foreign intelligence assesses, it hands the Kremlin a legal instrument to decide which companies survive the insolvency wave building inside Russia’s war economy—a state-run ver

Russia’s State Duma has passed the largest overhaul of its bankruptcy law since the statute was written. On paper, the reform saves jobs by favoring rescue over liquidation.

It hands the Kremlin a legal instrument to decide which companies survive the insolvency wave.

In practice, Ukraine’s foreign intelligence assesses, it hands the Kremlin a legal instrument to decide which companies survive the insolvency wave building inside Russia’s war economy—a state-run version of “too big to fail,” where Moscow writes the list.

The fine print lets Moscow overrule creditors

The scale explains the urgency. Russian companies now owe more than everything Russia’s economy produces annually: 293 trillion rubles ($3.85 trillion) in liabilities by the end of April, against a GDP of about 214 trillion rubles ($2.8 trillion). Overdue payments rose 18% in a year to 7 trillion rubles ($92 billion).

That unpaid sum equals roughly three-quarters of Russia’s official annual defense budget. More than a third of corporate profits now go to paying interest alone.

In a system where the biggest lenders are state banks, that lets Moscow impose survival on chosen enterprises.

The law flips the system’s default from liquidation to rescue. Companies gain a pre-bankruptcy sanation track to settle with creditors before any court case opens, plus a judicial debt-restructuring procedure with plans running up to four years, extendable by four more. A new anti-crisis manager oversees the debtor’s finances, payments, and recovery plan.

The decisive mechanism is the binding clause. For large debtors—companies with assets above 1 billion rubles ($13 million)—a court-approved sanation agreement, backed by a majority of independent creditors, becomes binding even on creditors who refuse to sign it. In a system where the biggest lenders are state banks, that lets Moscow impose survival on chosen enterprises and silence holdouts.

Six years of stalling ended in two days

Versions of this reform stalled for six years, with one government bill frozen in the Duma for two and a half years. Then the package cleared its second reading on 7 July and passed the third a day later.

“Its hasty advancement coincided with a sharp deterioration in Russian companies’ finances,” Ukraine’s Foreign Intelligence Service assessed on 13 July. The system being replaced rescued almost no one: external administration was applied in 51 cases in all of 2025, financial recovery in eight, and rehabilitation accounted for less than 1% of corporate bankruptcies.

Sberbank chief German Gref told shareholders in late June that investment had fallen more than 14% and could drop a further 3% this year.

The agency expects Moscow to apply the new mechanisms selectively—defense plants first, then critical infrastructure, large employers, and companies dependent on state orders—to stagger big insolvencies and keep distressed assets from flooding the market at once.

Russia’s own top financiers had already publicly linked the strain to the war. Sberbank chief German Gref told shareholders in late June that investment had fallen more than 14% and could drop a further 3% this year, while central bank governor Elvira Nabiullina’s Bank of Russia conceded that pro-inflationary risks had worsened.

Explore further

Russia’s top bankers break taboo, admit war is hurting the economy

The warnings are not only Ukrainian. In February, Ukrainian intelligence put non-performing loans above the 11% threshold that defines a systemic banking crisis, citing research on the $210–250 billion in loans Russian banks were forced to extend to defense contractors.

And a European intelligence note seen by Reuters warned on 6 July that the burden banks carry for the war economy creates an “explosive” risk—more than 500,000 Russians declared personal bankruptcy in 2025, up almost a third in a year.

Russian bankruptcy practitioners caution the new procedure works only if courts genuinely assess whether a business can recover.

Russian bankruptcy practitioners caution the new procedure works only if courts genuinely assess whether a business can recover—and with over a third of profits going to interest, many cannot. The law postpones the reckoning rather than canceling it.

Two of Russia's most senior economic figures publicly linked the country's mounting economic pressures to the war in Ukraine last week — an unusual departure from the official silence that has surrounded Kremlin war costs since 2022. German Gref, chief executive of Sberbank, and central bank governor Elvira Nabiullina both spoke in separate settings as Ukraine's drone strike campaign against Russian oil infrastructure compounds the fiscal strain from record military spendin

Two of Russia's most senior economic figures publicly linked the country's mounting economic pressures to the war in Ukraine last week — an unusual departure from the official silence that has surrounded Kremlin war costs since 2022. German Gref, chief executive of Sberbank, and central bank governor Elvira Nabiullina both spoke in separate settings as Ukraine's drone strike campaign against Russian oil infrastructure compounds the fiscal strain from record military spending.

Russia's military and classified spending reached 46% of all budget expenditure in the first quarter of 2026 — a surge of roughly 30% over the same period in 2025 — while the National Wealth Fund buffer has fallen from about 7% of GDP before the war to 1.7% as of April 2026, Russia's Finance Ministry confirmed.

What each of them said

Gref told Sberbank's annual shareholders meeting that investments had already fallen over 14% and could drop a further 3% this year. He then addressed the war directly.

"I don't believe there is anyone in this country whose primary concern is anything other than an end to military hostilities as soon as possible," Gref said.

For the chief executive of Russia's largest state-controlled bank to frame the war as the country's overriding problem — not "the special military operation," not a security challenge to be managed — marks a notable break from the language Kremlin officials have enforced since February 2022.

Nabiullina's public position is more constrained, but the Bank of Russia's own press release on her June rate decision said fiscal policy had become more accommodative than previously expected and that pro-inflationary risks had worsened — the same dynamic that Kluge's analysis traces directly to the gap between military outlays and tax revenues.

The fiscal picture behind the exchange

The 46% military spending figure comes from analyst Janis Kluge of the German Institute for International and Security Affairs, drawn from Finance Ministry data and cited by ISW. Russia is now covering an increasing share of the deficit through borrowing, with liquid National Wealth Fund assets depleted to a fraction of their pre-war level and no longer functioning as a meaningful cushion.

Ukraine's strike campaign is compressing the revenue side simultaneously. Bloomberg counted 38 Ukrainian strikes on Russian refineries from January through May 2026, with 16 in May alone — the highest monthly figure of the war. Two strikes on 16 and 18 June disabled both primary processing units at the Kapotnya refinery in Moscow — the capital's main fuel source — leaving it unable to process crude until at least early 2027.

Russia has responded by banning gasoline and jet fuel exports, drawing down strategic reserves, allowing lower-grade fuel blends, and importing gasoline from India and Belarus, while negotiations with Kazakhstan are complicated by the fact that a Ukrainian strike disrupted the feedstock supply to one potential Kazakh supplier.

Russian President Valdimir Putin publicly admitted queues at filling stations while summoning top officials to manage the crisis. Parliament passed legislation subsidizing gasoline imports from abroad.

The European Union renewed its economic sanctions on Russia for another 12 months, to 31 July 2027, the Council of the EU said on 25 June. The decision keeps the bloc's full economic regime against Moscow in place over the war on Ukraine. It follows the agreement EU leaders reached at their June summit.

The EU first imposed these economic measures in 2014 over Russia's full-scale invasion of Ukraine, then sharply widened them after the full-scale invasion in February 2022.

The European Union renewed its economic sanctions on Russia for another 12 months, to 31 July 2027, the Council of the EU said on 25 June. The decision keeps the bloc's full economic regime against Moscow in place over the war on Ukraine. It follows the agreement EU leaders reached at their June summit.

The EU first imposed these economic measures in 2014 over Russia's full-scale invasion of Ukraine, then sharply widened them after the full-scale invasion in February 2022. Brussels has cast the renewal as keeping pressure on Moscow until it stops the war and negotiates.

What the renewed measures cover

The sanctions span trade, finance, energy, and dual-use technology, the Council said. They include the ban on importing or transferring Russian seaborne crude oil and certain petroleum products into the EU.

They also bar transactions with several Russian financial institutions and crypto service providers, including some based in third countries, and suspend the broadcasting licenses of several Kremlin-backed disinformation outlets in the EU. Other tools let the bloc counter attempts to circumvent the sanctions.

The Council said the EU would keep the measures in place and stood ready to add more as long as Russia continues its war.

Explore further

Russia’s former soldiers may face a locked EU border—if France and Italy stop balking

Part of a wider sanctions push

The renewal builds on a regime that now spans 20 sanctions packages adopted since the February 2022 invasion. The bloc's leaders had agreed to the 12-month extension at the European Council on 18–19 June, when one member state's pro-Russian leader had vowed to veto the next batch.

EU leaders also called for swift adoption of a 21st sanctions package, aimed at further cutting Russia's energy revenue, curbing its shadow fleet, and constraining its banks. The renewal lands as enforcement draws scrutiny elsewhere: Washington has removed a string of Russians, ships, and firms from its own blacklist in recent months, giving no public reason.

Alongside the economic measures, the EU keeps separate restrictions on occupied Crimea, including Sevastopol, and on the Russian-occupied parts of the Donetsk, Kherson, Luhansk, and Zaporizhzhia oblasts, plus asset freezes and travel bans on a broad list of individuals and entities.

On 22 June, Volodymyr Zelenskyy signed a record budget of 4.4 trillion hryvnia ($97.6 billion), most of it borrowed from Europe. The money to keep Ukraine fighting, and eventually to rebuild it, is flowing as never before.

The constraint that now shapes Ukraine’s economic future is no longer money but the power, workers, and institutions to use it.

That same quarter, the economy it is meant to revive posted its sharpest contraction since the wartime recovery began—

On 22 June, Volodymyr Zelenskyysigned a record budget of 4.4 trillion hryvnia ($97.6 billion), most of it borrowed from Europe. The money to keep Ukraine fighting, and eventually to rebuild it, is flowing as never before.

The constraint that now shapes Ukraine’s economic future is no longer money but the power, workers, and institutions to use it.

That same quarter, the economy it is meant to revive posted its sharpest contraction since the wartime recovery began—and the constraint that now shapes Ukraine’s economic future is no longer money but the power, workers, and institutions to use it.

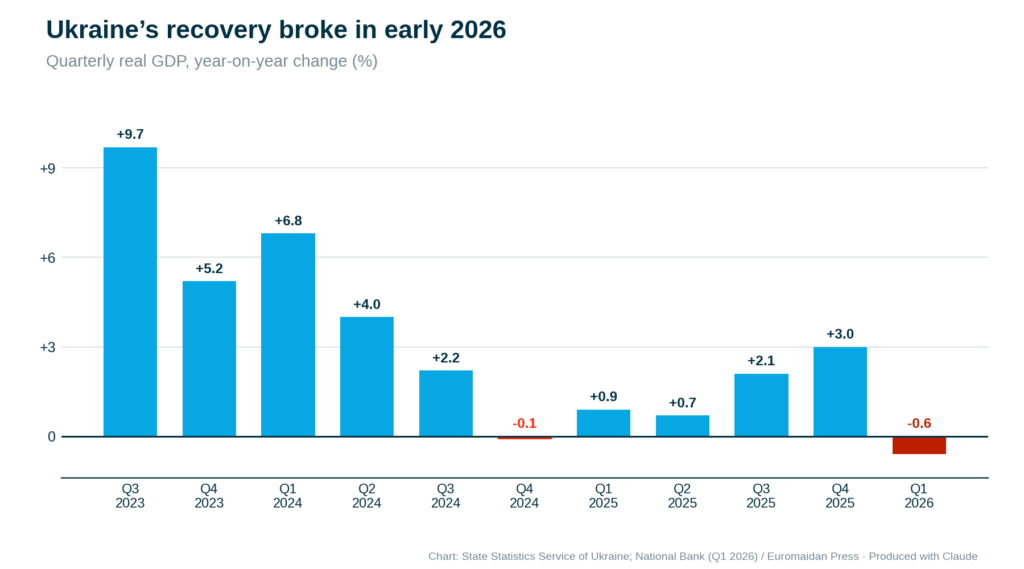

Real GDP fell 0.6% year-on-year in the first quarter of 2026, the National Bank confirmed on 18 June, and 0.7% against the previous quarter. The number is small. What hides behind it is not.

For nearly three years, Ukraine’s economy grew through bombardment—near-continuously from the middle of 2023, when the country clawed its way back from a collapse of almost 29% in the invasion year. It dipped only once before now, briefly, when drought hammered the harvest at the end of 2024. The first quarter of 2026 was the sharper break.

The investment house ICU said it bluntly: weak growth is “the new norm.”

The official line is more hopeful: the National Bank expects growth back as soon as the second quarter, and the government pencils in 4.5% for 2027. But a bounce off a depressed quarter is not a recovery, and the full-year number has only been marked down further.

After the recovery took hold in mid-2023, Ukraine’s economy grew nearly every quarter, dipping only once—a marginal 0.1% when drought gutted the 2024 harvest. Russia’s strike campaign then pushed it down 0.6% year-on-year in the first quarter of 2026. Chart: State Statistics Service of Ukraine; National Bank of Ukraine / Euromaidan Press. Produced with Claude

Where the bombs show up in the accounts

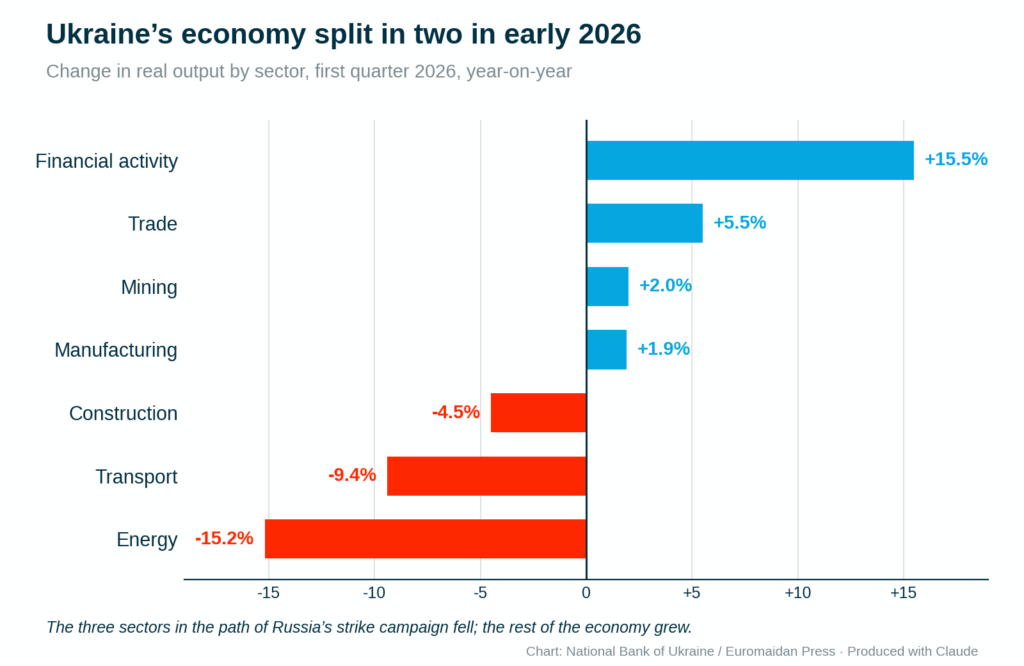

The contraction has a clear author. Energy output fell 15.2% year-on-year, transport 9.4%, and construction 4.5%, the National Bank’s breakdown showed—the sectors directly in the path of the strike campaign, now showing up as line items in the national accounts.

The economy contracted because three bombed sectors outweighed a domestic economy that kept working.

The first sector to fall was electricity generation, with transmission disrupted where the grid was hit; the second was transport, after heavy strikes on the railways, economist Oleksandra Betliy told Kyiv Post.

Household consumption rose 11%. Manufacturing grew 1.9%, trade 5.5%, financial activity 15.5%, and mining 2%. The economy contracted because three bombed sectors outweighed a domestic economy that, by almost every other measure, kept working. ICU called the quarter a display of “unprecedented resilience” to the blackouts.

The hryvnia keeps sliding

Unlike the contraction, the hryvnia's slide owes nothing to the weather. Through the first five months of 2026, the hryvnia weakened against the National Bank’s official rate—from a 2025 average of 41.7 to the dollar to 42.9 in January, 44.1 by May, and 44.9 by 23 June. A widening trade gap drives the slide, the Centre for Economic Strategy reported.

A cold snap can knock out a quarter of GDP growth. It cannot make a currency depreciate every month for half a year. That slide tracks a structural deficit between what Ukraine earns abroad and what it spends there, and it will outlast the spring.

Reserves dropped to $45.7 billion by the start of June.

Defending that slide has cost the central bank its cushion. Reserves dropped to $45.7 billion by the start of June, down from a record near $57.7 billion early in the year—roughly $12 billion sold off in four months to slow the hryvnia while partner aid ran late. The National Bank calls the level sufficient, about 4.7 months of imports, and the inflows now arriving are meant to refill it.

Prices, at least, are easing. Inflation slowed to 8.2% in May, helped by falling oil prices as the war in the Middle East de-escalated—Washington cleared Iranian crude sales on 22 June, pushing prices to around $74 a barrel, which both cheapens Ukraine’s energy imports and thins Russia’s war revenue. The National Bank held its key rate at 15% on 18 June, judging the easing cycle done for now.

The contraction came from three sectors, not the whole economy. Energy, transport, and construction—the parts directly in the path of Russia’s strikes—fell sharply in the first quarter of 2026, while financial activity, trade, mining, and manufacturing kept growing. Chart: National Bank of Ukraine / Euromaidan Press. Produced with Claude

The deeper drag

The contraction had near-term authors—the strikes, the cold, the delayed budget spending. The drag beneath them is older, and no thaw fixes it: Ukraine is running out of people. The number of full-time employees fell from 7 million in 2021 to 5.3 million by late 2025, according to GMK Center, citing official data.

The shortage pushes wages up even as output falls—part of why inflation has stayed above 8%.

Half of companies were already citing the staff shortage as the main obstacle to their businesses six months ago, Euromaidan Press reported, citing the National Bank’s enterprise survey, and the labor force has only thinned since then.

The war took around a quarter of the labor force; 5.9 million Ukrainians are abroad; and the National Bank expects the net outflow to run into 2027 before any return begins. The shortage pushes wages up even as output falls—part of why inflation has stayed above 8%, and a large part of why every forecaster now caps growth near zero.

Explore further

How Ukraine’s economy survived four years of war—and what it cost

Money is arriving

For most of the war, the binding question was whether the money would come at all. In February, it nearly didn’t: Hungary’s Viktor Orbán blocked the €90 billion ($104 billion) EU loan agreed in December, holding it hostage to a dispute over Russian oil through the Druzhba pipeline.

Then Orbán lost his election after 16 years; his successor dropped the obstruction; the pipeline was repaired; and the bloc finally approved the package on 23 April—€45 billion ($52 billion) of it for 2026.

The inflows have a paradoxical effect on the books: the projected 2026 deficit has narrowed to 12.1% of GDP.

That money is what funds the record defense budget. The first €3.2 billion ($3.7 billion) tranche of budget support lands at the Recovery Conference in Gdańsk on 25–26 June, with €5.9 billion ($6.8 billion) for the army to follow by the end of the month, European Pravda reported.

The central bank expects roughly $13 billion in June across all programs. The inflows have a paradoxical effect on the books: the projected 2026 deficit has narrowed to 12.1% of GDP, from the 18.5% first planned, the Centre for Economic Strategy noted in the same review, though defense spending is running at only about 80% of plan, and the budget underfunded the military pay raises it promised.

The bind is no longer the money

The bill, as of December 2025, is almost $588 billion—nearly three times the country’s annual output—a joint assessment estimated by the World Bank, EU, and UN in February, up from the $524 billion figure of a year earlier.

$20 billion to replace destroyed capital, $10 billion to stop falling further behind its eastern European peers, and $10 billion to start closing the gap.

To rebuild and keep pace with its neighbors, Ukraine needs around $40 billion a year, the Berkeley economists Yuriy Gorodnichenko and Maurice Obstfeld estimate: $20 billion to replace destroyed capital, $10 billion to stop falling further behind its eastern European peers, and $10 billion to start closing the gap. Set against Poland’s post-communist investment inflows, or the immobilized Russian assets sitting in Europe, that figure is not a fantasy.

The problem is the other side of the ledger. Ukraine can realistically absorb $10 to 15 billion a year right now, Ukraine’s deputy representative at the IMF, Vladyslav Rashkovan, arguedon a Centre for Economic Strategy podcast.

If $100 billion arrived this month, he said, the country could not spend it. Not enough projects are ready. Not enough institutions to run them. Not enough throughput at a customs service that would have to clear 10 times the imports.

The question now is whether Ukraine can build the capacity to take the funding.

The workers to do the rebuilding are scarcer still: around 4.5 million will be needed, the Economy Ministry projectedalready in January, in an economy already short more than 600,000 skilled hands this year.

The constraint has quietly flipped. For three years, the question was whether the world would fund Ukraine. The question now is whether Ukraine can build the capacity to take the funding—and that is slower, less photogenic work than wiring a loan.

It is also the work that decides everything downstream. Investment does not go where a president points it, Rashkovan said; it goes where the balance of risk and return beats the alternatives. The institutions, the rule of law, the energy capacity to power a rebuilt economy, the workers to build it—none of it visible, all of it now the binding constraint on whether the recovery resumes or settles into the new normal ICU described.

Ukraine has $5.8 billion lined up for priority reconstruction projects this year, and a $9.5 billion funding gap remains.

The contraction may not be the most important number from this June. Ukraine has $5.8 billion lined up for priority reconstruction projects this year, and a $9.5 billion funding gap remains. The bombs are still landing on the sectors that fell. And the hryvnia, indifferent to the weather, keeps closing on 45.