Ukraine reaches Russian oil platforms in "safe rear areas". Ukrainian long-range drones, operated by the Alpha Special Operations Center of the Security Service (SBU), have struck oil production platforms owned by Lukoil-Nizhnevolzhskneft in the Caspian Sea for the third time in the past week, UkrInform reports.

On 11 and 12 December, SBU drones had already hit the Filanovsky and Korchagin platforms. The Filanovsky field is one of the largest discovered in Russia and in it

Ukraine reaches Russian oil platforms in "safe rear areas". Ukrainian long-range drones, operated by the Alpha Special Operations Center of the Security Service (SBU), have struck oil production platforms owned by Lukoil-Nizhnevolzhskneft in the Caspian Sea for the third time in the past week, UkrInform reports.

On 11 and 12 December, SBU drones had already hit the Filanovsky and Korchagin platforms. The Filanovsky field is one of the largest discovered in Russia and in its sector of the Caspian Sea, with estimated reserves of 129 million tons of oil and 30 billion cubic meters of gas.

This time, the strike targeted a platform at the Korchagin oil and gas condensate field. According to the source, the drones damaged critical equipment, resulting in a complete halt of production processes at the site.

Striking oil revenues as a weapon of war

The Security Service of Ukraine emphasizes that such operations are part of a systematic effort to reduce the flow of oil revenues into Russia’s budget.

These funds are used to finance the war against Ukraine, from missile production to sustaining the army.

“No Russian facility that supports the war effort is safe, regardless of its location,” the SBU source said.

Ukraine is increasingly pushing combat operations deep into Russia's rear, undermining its capacity to wage war.

Ukraine adopted restrictions on 26 Russian energy companies, including oil giants Rosneft and Lukoil, on 30 November, synchronizing its sanctions with the United States, President Volodymyr Zelenskyy announced.

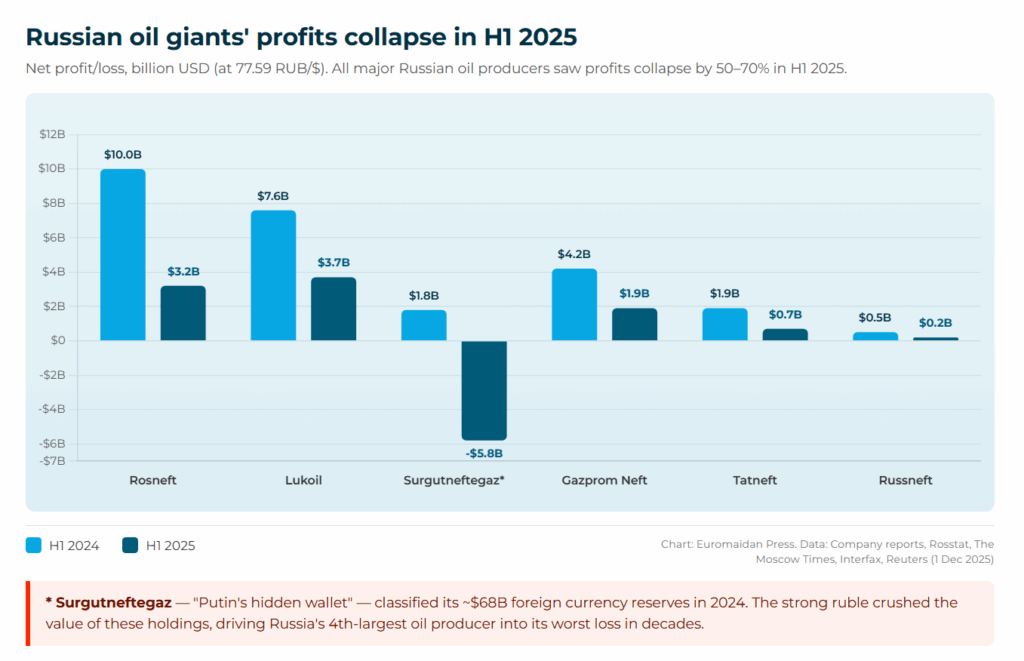

The move comes as Russia’s oil sector buckles under sustained pressure: nearly half of Russian oil companies—48.1%—operated at a loss in the first three quarters of 2025, Rosstat data cited by The Moscow Times shows. Rosneft itself lost two-thirds of its profit i

Ukraine adopted restrictions on 26 Russian energy companies, including oil giants Rosneft and Lukoil, on 30 November, synchronizing its sanctions with the United States, President Volodymyr Zelenskyy announced.

The move comes as Russia’s oil sector buckles under sustained pressure: nearly half of Russian oil companies—48.1%—operated at a loss in the first three quarters of 2025, Rosstat data cited by The Moscow Times shows. Rosneft itself lost two-thirds of its profit in the first half of 2025.

Sanctions pressure tightens

The US Treasury originally designated Rosneft and Lukoil on 22 October, with restrictions taking effect on 21 November. Together, the two companies account for roughly 55% of Russia’s oil production. Russian crude prices fell to multi-year lows following the designations, with major Indian and Chinese buyers pausing purchases.

For the first eleven months of 2025, Russia’s energy revenues have fallen 22% to approximately $102 billion, down from $141 billion in the same period last year.

The broader Russian economy is showing strain.

About a quarter of Russian firms with outstanding bank loans are now behind on payments—the highest share in at least 2.5 years, according to Central Bank statistics cited by The Moscow Times. Business investment has also weakened, with capital expenditure growth slowing almost sixfold from 8.7% in the first quarter to 1.5% in the second.

Kyiv signals alignment with Washington

Ukraine’s adoption marks its 13th synchronized sanctions package with Western partners this year, including the UK, Canada, Japan, and the EU.

The timing is noteworthy: the announcement came the same day Ukrainian and American delegations held talks in Miami.

Although no sources mention the sanctions being the topic of the negotiations, the synchronization signals Kyiv’s effort to demonstrate its value as a coordinated partner, even as ceasefire negotiations remain uncertain.

Presidential sanctions adviser Vladyslav Vlasiuk said pressure on Russia must increase through year-end, with priorities including further coordination with partners and preparation of the EU’s 20th sanctions package.

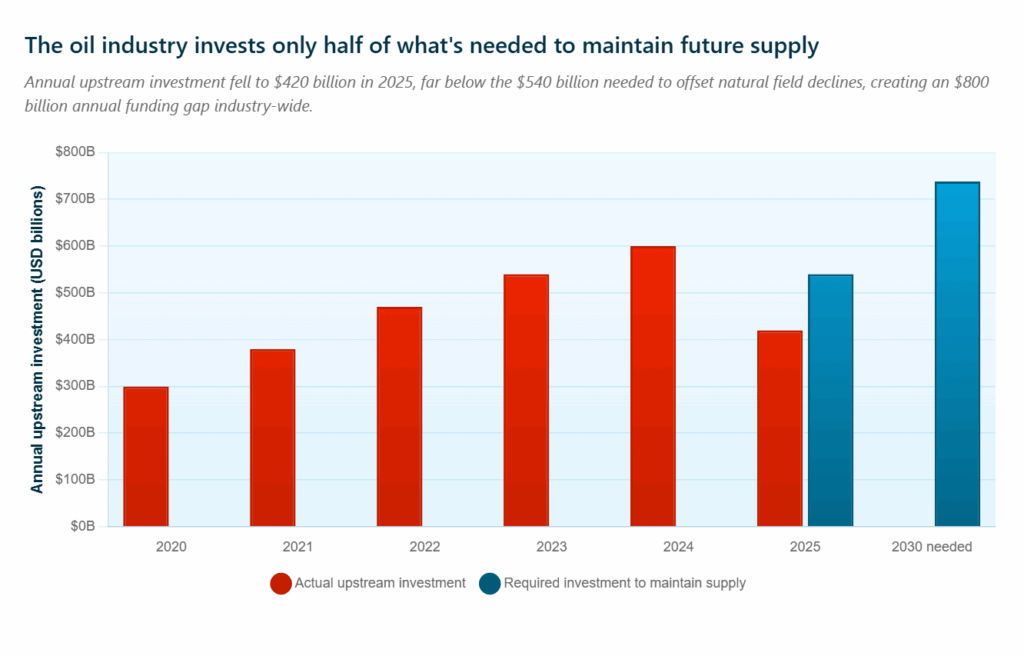

Oil prices dipped to $63.10 per barrel Tuesday as Deutsche Bank forecast a 2-million-barrel-per-day surplus in 2026, but this short-term glut masks a structural crisis: the global oil industry is chronically underinvesting by roughly $800 billion annually—about $2.2 billion every single day—even as natural field declines require 5 million barrels per day of new production yearly to hold output flat.

Russia’s sanctions-induced production collapse compounds the timeline.

Oil prices dipped to $63.10 per barrel Tuesday as Deutsche Bank forecast a 2-million-barrel-per-day surplus in 2026, but this short-term glut masks a structural crisis: the global oil industry is chronically underinvesting by roughly $800 billion annually—about $2.2 billion every single day—even as natural field declines require 5 million barrels per day of new production yearly to hold output flat.

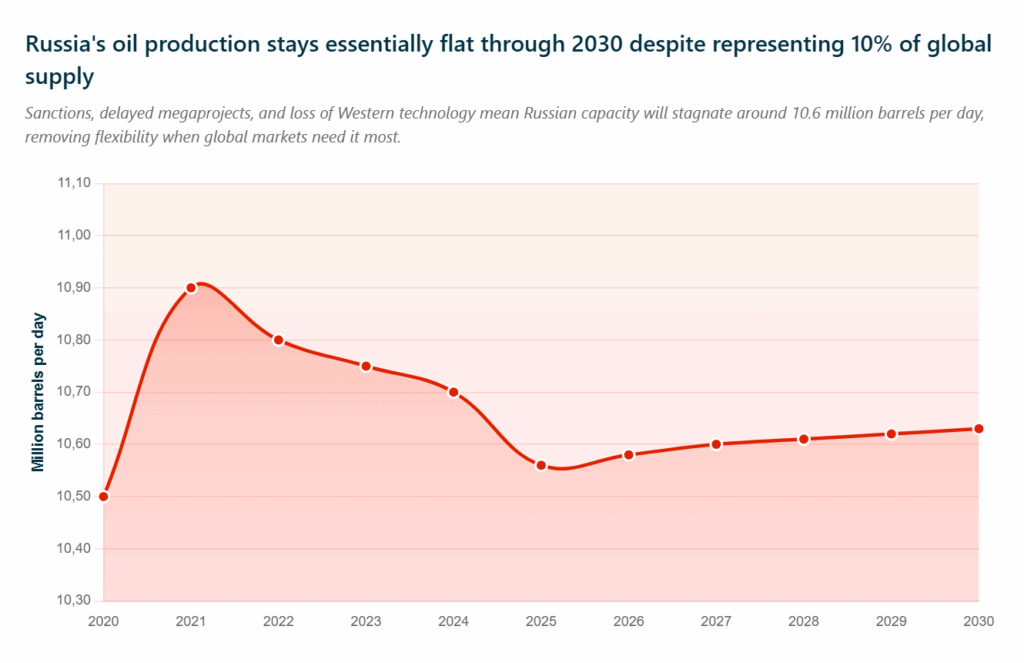

Russia’s sanctions-induced production collapse compounds the timeline.

Russian output fell to 10.70 million barrels per day in 2024, with the International Energy Agency’s forecast showing a further decline to 10.56 million barrels in 2025 and only 10.63 million by 2030—essentially flat, despite Russia representing roughly 10% of global supply.

The massive Vostok Oil project, intended to add 600,000 barrels per day, has been delayed from 2024 to 2026, while Arctic LNG-2 has been scaled back, with its timeline pushed from 2026 to 2028.

The investment crisis hits precisely when global supply needs every available barrel. Industry executives have reported investing only 50% of the necessary capital for over a decade, Eni CEO Claudio Descalzi told the recent ADIPEC conference. Exploration and production investment is falling 6% to around $420 billion in 2025—well below what’s needed to maintain future capacity.

Today’s surplus is tomorrow’s shortage

Conventional oil reserves naturally decline at a rate of around 6% per year, requiring continuous capital deployment to maintain production capacity. The IEA projects that supply capacity growth will reach 1.8 million barrels per day in 2025, then transition to contraction after 2029 as the pipeline of non-OPEC+ projects wanes after 2027.

The current oversupply exists because the global recession has crushed demand, not because supply is abundant to meet future requirements.

If OPEC+ sustains current production rates, global supply could reach 107.2 million barrels daily by 2030—1.7 million barrels higher than projected demand, according to IEA data. Yet this near-term surplus masks post-2027 capacity constraints.

To stem output losses at producing fields, well capital expenditures and field direct operating costs reached nearly 90% of their 2014 highs in 2024—the third-highest level in industry history, IEA reports. These investments are required to maintain the existing supply as natural decline rates erode production capacity.

Investment mandates prioritizing environmental and social criteria now direct two-thirds of the $3 trillion annual energy investment toward renewables.

Major pension funds, including CalPERS and ABP, have implemented divestment policies for fossil fuels, while banking institutions have withdrawn financing for new petroleum developments.

This has created a 2-to-1 capital ratio favoring renewables over fossil fuels, up from roughly a 1-to-1 ratio a decade ago—the result is capital restrictions that persist regardless of price signals that would traditionally spur investment.

Russia’s oil output stays frozen at 10.6 million barrels per day through 2030 as sanctions block Western technology and key projects stall, removing a critical supply buffer from global markets. Chart: IEA / Euromaidan Press

Russia’s permanent capacity loss

Western sanctions have devastated Russia’s ability to maintain production infrastructure. War and economic impact have held back Russian investment due to all-time high interest rates, higher corporate taxation, and tight labor markets, while sanctions restrict access to technologies, financing, and supply chain inputs.

Russian crude capacity is projected to fall from 9.53 million barrels daily in 2024 to 9.47 million by 2030. Russia’s inability to access Western drilling technology and spare parts means its production capacity is eroding even as it maintains current output by depleting reserves faster—borrowing from future supply to meet today’s quotas.

Delayed megaprojects, declining field capacity, and technological restrictions ensure that Russian supply won’t recover to pre-war levels even if sanctions are lifted.

Explore further

Russian refinery shuts down as repair crisis deepens

The service sector can’t respond quickly

The petroleum service industry faces severe capacity constraints after years of reduced activity. When operators eventually seek to increase drilling, they’ll encounter equipment shortages for modern drilling rigs, workforce limitations from reduced training programs, and extended lead times for specialized systems throughout the supply chain.

These bottlenecks limit rapid response to demand recovery or geopolitical disruptions, even when prices justify increased production.

The shift from conventional to unconventional production has changed industry response times. Conventional oil fields show annual decline rates of 5-15%, with development timelines spanning 5-10 years.

Unconventional shale operations face first-year decline rates of 40-70%, with development compressed to 6-12 months but peak production windows limited to 3-5 years. Shale’s rapid decline rates demand continuous drilling to maintain output, while conventional projects need long lead times that make quick supply responses impossible.

The coming squeeze

For energy-importing nations, current low prices offer false comfort. The structural investment deficit, combined with Russia’s eroding production capacity, creates vulnerabilities that could manifest in supply disruptions and price spikes when post-recession growth recovers after 2027.

The contradiction in today’s market: traders worry about 2026 oversupply, while supply capacity growth will contract after 2029. Major national oil companies illustrate the scale of capital required: Saudi Aramco increased its upstream spending by 19% to $39 billion in 2024, while Abu Dhabi’s ADNOC plans to spend $150 billion between 2024 and 2027 to achieve a crude supply capacity target of 5 million barrels per day by 2027, according to IEA data.

The timing of capacity constraints—supply growth peaking around 2027 before contracting after 2029—gives the industry a narrow window to address investment deficits before structural shortages emerge.

The oil market’s hidden crisis isn’t about today’s balance sheets—it’s about the supply capacity that won’t exist in 2029 because of investment decisions not made in 2024. Russia’s sanctions-induced collapse is bringing that reckoning closer.